I still remember the day I received my first credit card. It was on 21 August 2013. I was scheduled to fly to Taiwan. My maiden trip there. I received a call that my cards were ready early in the morning and made my way to Maybank's Johor Jaya branch to pick them up.

It was the entry-level Maybank 2 Gold with a starter credit limit of RM5,000. Just nice for a guy in his early 20s. In my mind I went "Oh wow, this arrived at the PERFECT timing, just hours before my long-awaited vacation!" and rushed home to do some last minute packing before my evening flight.

You know how the story went. Just like how any other younglings ended up after they were first bestowed with the power of credit. I went on a spending spree in Taiwan. Charging meals, attraction entrance fees, shopping purchases & more to the card. Things that I would normally buy. Things that I wouldn't normally buy. It was so easy to spend, thinking that I would just settle it later on. I ended up racking bills of close to RM4,000+. Very very close to the limit. Took me 2-3 months after the trip to clear it off.

The first few years of owning a credit card were filled with anxiety. I was stuck in a cycle of clearing off & racking up balances again & again. A never-ending hole. Of course, I got better after I decided to beat the "game". Now I enjoy lots of perks. No more interest payments & bad feelings.

The Proper Way to Use a Credit Card

It took me a few years to learn the proper way to use a credit card. The basics/straightforward stuffs being:

1. Spend within your means. Only charge necessary expenses to the card. Stuffs like food, groceries, petrol, shopping, utilities, that you would normally pay with cash

2. Know when to pay by knowing the key dates

3. Charge as much as possible (keep in mind point #1) to rack up credit card points

4. Know the perks of your credit card

5. Say no to cash loans

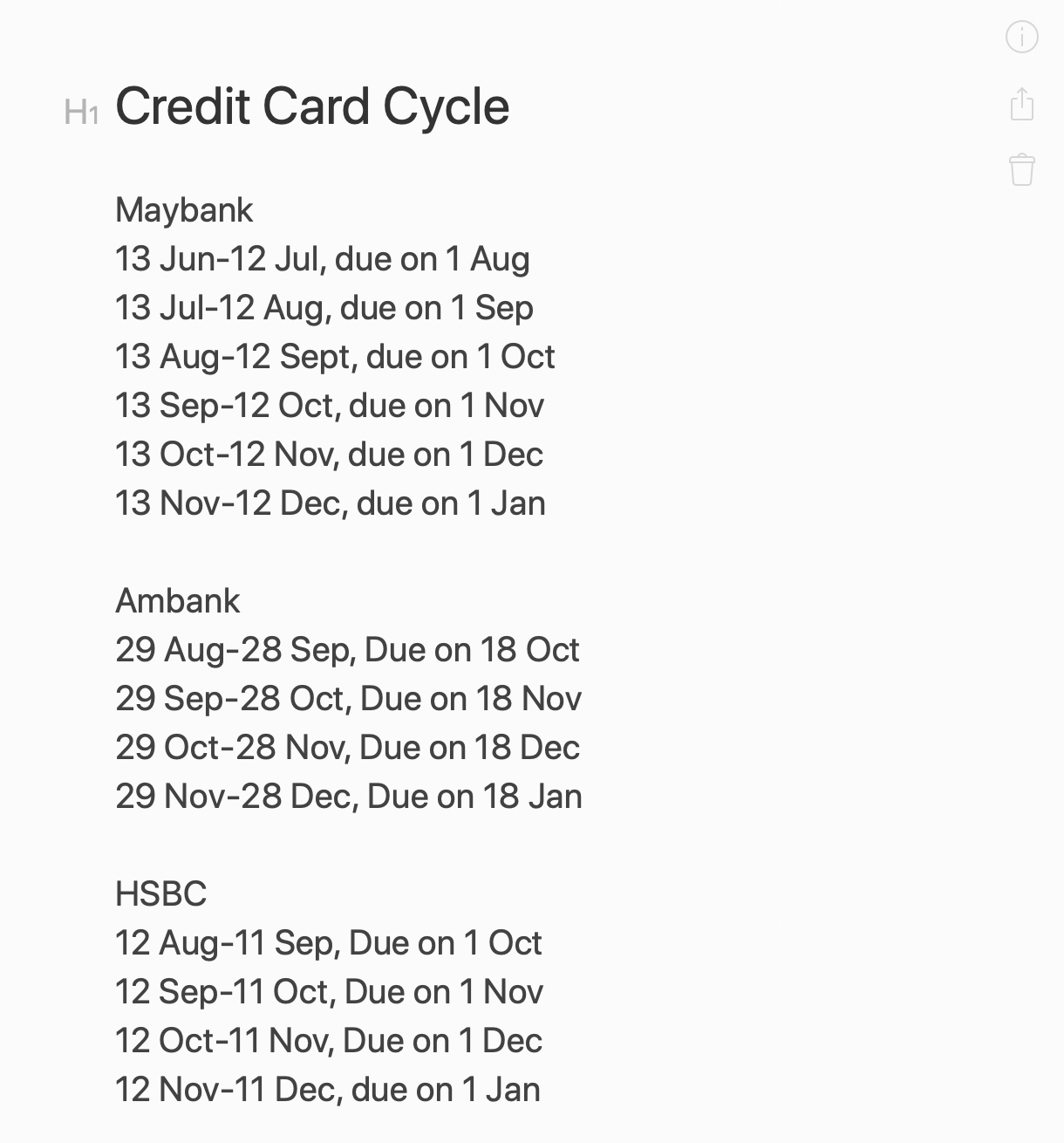

The most important tip would be understanding the key dates of a credit card. Most banks give a 21-days interest free period from the statement date. The statement date is the last day of a 30-days billing cycle. If you time your expenses properly, you can actually get an interest free float of up to 50 days. Let me use real dates from one of my credit card statements to illustrate a concrete example:

Statement Date: 12 October 2019

Due Date: 1 November 2019

Statement Period: 30 days (13 September to 12 October 2019)

In other words, if I make a purchase on 13 September 2019, I will have 50 days to pay it off. 49 days for 12 September's expenses and so forth. By understanding my Statement Period (30 days with Statement Date being the last day) and paying only on the Due Date itself, I will be able to create an interest-free float.

What's the big deal with that? Well, it means that the cash can be redeployed to an interest-bearing account to generate free money. The sum might be small, but it's free for the taking and it reduces anxiety when you know exactly when to pay. Now, if you use the same tactic for your business expenses, you will be able to generate a substantial float and free up cashflow.

It can get confusing to keep track of the various dates. Thus in my phone's note, I track it via the dummy way:

The Best Credit Card Combo in Malaysia

Now, what are the credit cards that I recommend? I used to apply for a lot of cards, but I've come to realise it's a hassle to keep track of multiple statement periods & due dates. Now I only use a main card together with a few backup cards:

Main Card (for daily spendings)

1. Maybank 2 Card Premier. The best credit card in Malaysia hands down. Accumulates air miles the fastest. Effectively a 20-30% cashback on your spending when you convert the points to air miles and do business class flight redemptions. Read the guide I wrote here. 5x complimentary lounge access. RM800 annual fee, waived for spending of RM80,000 and above per annum.

Backup Cards (for emergency in case main card is maxed out)

1. Ambank "Duo" (Conventional World Mastercard & Islamic Visa Infinite). Separate credit limit for conventional & islamic cards. 5x complimentary lounge access per card. Free for life with no minimum spend; rare for premier cards. Get both if you qualify.

2. HSBC Visa Signature: nothing special besides the 6x complimentary lounge access and nice card design. Swipe once a month for annual fee waiver. Got it as HSBC had a RM250 cashback promo. Decided to keep it as backup credit

3. BigPay: not a credit card, but a great card for oversea ATM withdrawal due to its low fees & good conversion rates

Together they form my ultimate credit card stack in Malaysia. Combine with the usage tips above, I hope you will be able to get the most out of your cards. Happy credit card hacking!